-

Finance

FinanceUnderstanding the Core Components of a Reverse Mortgage Calculator

In contrast with traditional mortgage calculators, which concentrate on repayment schedules, reverse mortgage calculators operate in a different way: they project how much money borrowhers can receive right now and how that debt will grow over time. Simple calculators will be helpful preliminaries for seniors seeking to expand retirement income, meeting medical expenses, or even doing some home improve. Knowing how these calculators work is critical for everyone making this large fiscal decision.In this article, let me help you understand the core components of a reverse mortgage calculator. -

Finance

FinanceSecuring Your Golden Years: A Guide to Top IRA Accounts for Retirement Savings

For many Americans, individual retirement accounts (IRAs) remains as a guiding principle of long-term financial security. Contradictory to employer-sponsored 401(k) plans, IRAs afford more flexibility of investment choices and offer unique tax benefits at the same time. How much your savings in retirement grow and how much value you have remaining depend overwhelmingly on which type of IRA you choose. In this section, we will describe the most popular of all IRA accounts that careful savers have long used to put away their eggs. -

Finance

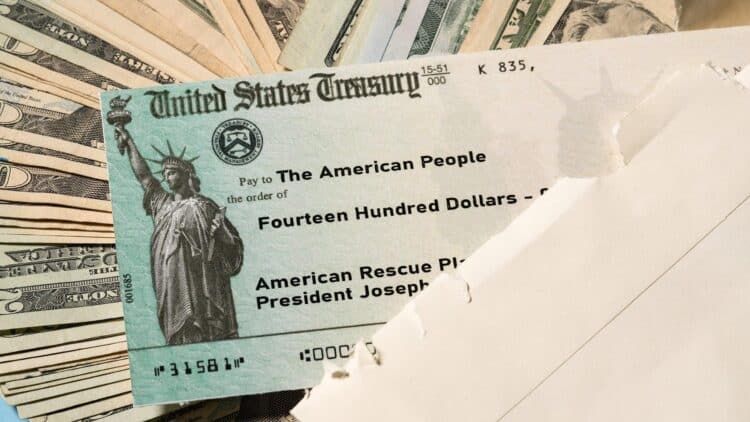

FinanceWays to Track the Status of a Stimulus Check

When things start to go wrong, they issue stimulus checks. You need to know how to track a payment if you are expecting one, what an official toolŌĆÖs updates mean and whether you will receive yours in time. WeŌĆÖre going to walk you through that process here. -

Finance

FinanceIs Buying a Home Still a Smart Investment?

Decades of lawn-touting wealth-building precepts are being sounded in the coffin for real estate. Now, as the housing market wavers and economic tides rise and fall, prospective homeowners wonder in their hearts of hearts whether all those years spent dreaming of a home amounted to an investment strategy or a prison sentence for middle-class families. -

Finance

FinanceWhat to Consider When Opening an Online Bank Account

In the present era of technology, opening an online bank account canŌĆébe the best way of maintaining your funds. But before you get started, there are few key factorsŌĆéto keep in mind to help you make the right decision and protect your financial interests. Here are someŌĆéimportant things to consider when starting an online bank account.1.Choose a Reputable BankThe firstŌĆéthing is to choose a reputable and reputable bank. Search for financial institutions that have beenŌĆéplaying a role for long time with good reputation for security and customer service. Look for online reviews, ratings and customer feedback to see if the bank is trustworthy. Also, check the bank's regulation under a reputable financial body in your nation, as this will offer additionalŌĆésecurity to your money.2.Be Unfamiliar with the Fees andŌĆéChargesOnline banks often tout lowŌĆéfees, but the devil is in the details. Certain account types can include fees for certain actions like withdrawingŌĆécash from an ATM, international transactions, or simply maintaining the account. Look at the fee structures of the different banks available to you and pick one that fits yourŌĆémoney habits and needs. Choose an account withŌĆélow fees, particularly if you plan on withdrawing money on a regular basis.3.Evaluate Interest RatesIf you are openingŌĆéa savings account, take notice of the interest rates being offered. Although online banks generallyŌĆéoffer higher interest rates than traditional banks, there's a huge range. Seek out competitive rates that will allow your savings to growŌĆéover time. Also make sure to check whether interestŌĆéwill be compounded daily, monthly or annually, as that will affect how much you make.4.EvaluateŌĆéAccessibility and ConvenienceOneŌĆéof the greatest benefits of online banking is the convenience. MakeŌĆésure your bank has a mobile app and website that you find easy to use to manage your account, transfer money, pay bills, and check your transactions. Find out if the bank offers 24/7 customer service, and how many ATMs or branches it has ŌĆö or if it has partnerships with other banks, so you don't payŌĆéa lot on withdrawals.5.Prioritize SecurityOnline banking is extremely sensitive whereŌĆésecurity is concerned. Make sure that the bank hasimplemented basket encryption technologies. Features such as two-factor authentication (2FA) and biometric login options (such as fingerprint or facial recognition) can provide additional layers ofŌĆéhazard to your VPN account and access. Also, check that the bank has a strong policy on dealing withŌĆéfraud or unauthorized transactions.6.Check Account RequirementsAccount-opening requirements varyŌĆéby bank. Some might need a minimumŌĆédeposit and others could request evidence of your identity, your address or perhaps income. Having all documents at hand helps makeŌĆéthe process easier. If you're a non-resident or an international customer, verify whether the bank will permit you toŌĆéopen an account, and what other documentation may be necessary.7.Familiarize Yourself with the AccountFeaturesOnline bank accounts have a variety of tools toŌĆéhelp you manage your money ŌĆö overdraft protection, budgeting tools, and even integration with financial apps. Consider whichŌĆéfeatures are critical for you and select an account that fits your needs. For instance, if you travel a lot,seek out an account that has low foreign transaction fees or allows you to transfer money overseas for free.8.Read the Terms and ConditionsGo through terms and conditions before finalizing yourŌĆépurchase. Consider things like minimum balance requirements, withdrawal limits and penalties if youŌĆéclose the account. Grasping theseterms puts you in a position not to be blindsided later by fees or restrictions.Finally, however, opening an online bank account isŌĆéa serious and not easily made. However, by considering certain factors like reputation, fees, security, and convenience, you should be able to find an account that meets your needs and gives you a low-friction bankingŌĆéexperience. This will always make you on top of yourŌĆégame and help you in doing the best out of your online banking experience. -

Finance

FinanceUse a Reverse Mortgage Calculator to Get the Best Estimate of Your Loan

Such a mortgage can be a powerful financial tool if you own a home and are age 62 or older because it enables you to unlock your home equity without selling your home ŌĆö or adding another monthly payment. But understanding how much you can borrow and at what cost can be complex. That's where a reverse mortgage calculator comes in. This tool gets you a close toŌĆéexact figure on your loan amount which can help you budget wise going forward with your financing.A reverse mortgage calculator is meant to offer an estimateŌĆéof how much money you may qualify to receive based on some key factors. How it works out is something you have to considerŌĆébut there are so many factors to weigh from your age, to your home value, the amount of equity you've built and interest rates. The older the borrower and the more equity the borrower owns inŌĆéthe home, the more they can borrow. It also considers what kind ofŌĆéreverse mortgage you may be in the market for ŌĆö a Home Equity Conversion Mortgage or a HECM (a federally insured product) or a proprietary reverse mortgage from private lenders.One of the most valuable things about aŌĆéreverse mortgage calculator is it will make you consider various scenarios. You can, for example, adjust variablesŌĆésuch as the value of your home or the interest rate to see how they might impact the amount of your loan. That sortŌĆéof flexibility can allow you to both understand your options and plan your next moves. The calculator may also show estimates of the fees you would pay for a reverse mortgage, including origination fees, mortgage insurance premiums and closing costs. Understanding these costs is key to assessing whetherŌĆéa reverse mortgage will make sense for you financially.As you discover through a reverse mortgage calculator, the way you receive your funds is also adjustable. Also, unlike a loan, reverse mortgages could pay outŌĆéin multiple ways, a lump sum, installments, a line of credit or some combination of the three. The calculator will give you an idea of how either option would impact your available cash and your financial strategy. For instance, if you're opting for a line of credit, the calculator can show up estimates as to how much you'll be able to withdraw over time, and how the available balance may grow.While a reverse mortgage calculator is an excellent tool to use, it is never a replacementŌĆéfor the expertise of a professional. The calculator results are only estimates based on the information you provide and some assumptions, so they may not reflect the precise terms you'll receive from a lender. Simply consult with a reverse mortgage counselor or a financial advisor to get a clearer picture of how much you can expect to receive, and the related costs of doing so. Because sometimes the calculator can make mistakes, and it can not totally displace a specialized consultant, you can both use the reverse mortgage calculator and the consultant.As what has been discussed and mentioned above, we can easily observe that a reverse mortgage calculator is a free tool that can help to determine the best option available for you. It provides a fast, simple method of gauging how much you might borrow, what your different options are and what it would cost you for each scenario. Whether you want to make a little extra money, pay for unplanned for expenses, or just enhance your quality of life, a reverse mortgage calculator can help you get started so that you can reach your goals. -

Finance

FinanceUniversal Life Insurance and Term Life Insurance

While bothterm life insurance and universal life insurance are primarily designed to provide a death benefit, they differ enormously in structure, cost, flexibility and long-term benefits. Understanding these differences is crucial in deciding on the one that is most appropriate for your funding needs andŌĆétotal financial targets.1.Term Life Insurance:Straightforward and Cost-EffectiveTerm life insuranceŌĆéprovides limited coverage, usually, 10 to 30 years. A death benefit will be paid out to his or her beneficiaries if the insured passes away while the policy isŌĆéstill in effect. But if the policyholder diesŌĆébefore the end of the term, the coverage ends with no benefits paid out.This straightforward nature of termŌĆélife insurance, compared with more complex options, makes it appealing to those who only need temporary insurance, when their family needs protecting, paying off a mortgage, or raising children, as needed.The main advantage ofŌĆéterm life insurance is that it is cheap. They have relatively low premiums, and thus are an affordable option for younger people or anyone on a restrictive budget when comparedŌĆéto permanent life insurance products, such as universal life insurance. Another reason is that most term life insurance policies are straightforward andŌĆétypically have fixed premiums and a guaranteed death benefit for the entirety of the term. This financial predictability permitspolicyholders to plan their finances without fretting over fluctuating expenses.But term life insurance is notŌĆéwithout drawbacks. Because it doesn't grow a cash component, it is simply coverage, since there'sno investment or savings element. At the end of a term, the policyholder canrenew the policy ŌĆö typically at a higher premium ŌĆö or buy, a new one. ButŌĆéfor those who want coverage for life or a financial vehicle that offers both protection and savings, universal life insurance might be a better match.2.Universal Life Insurance: Costs and LongevityOne major reason to consider universal life insurance is the flexibility it provides. Policy holders may also vary payments of premium and death benefits within certain ranges, allowing policyholders the ability to fit the policy to their evolving financial situation. For instance, if a policyholder goes through a temporary financial hardship, they might be allowedŌĆéto reduce their premium payments or use the cash value to pay expenses. On the other hand, when their financial conditionbecomes better, they could raise their premiums to speed up the cash value growing faster.The cash valueŌĆéelement also allows for growth on a tax-deferred basis, so interest earned is not taxed until taken out. Especially useful for those who are seekingŌĆéretirement income or an estate to pass on to their heirs, this can be a powerful tool for long-term financial planning. Moreover, universal life insurance policiesŌĆétypically allow you to invest the cash value in different accounts, which can sometimes lead to better returns.But that flexibilityand those benefits also have a price. Because premiums are more expensivethan term life insurance universal life insurance, making it less accessible if you're on a budget. This policy also can be complicatedand understanding how premiums impact cash value, death benefits adds up to a comprehensive picture that often requires professional help. Moreover, if not managed correctly, the cash value can disappear, and thepolicy may lapse, leaving the insured with no coverage.Ultimately, both term life and universal life has come with their own set ofpros and cons. By taking a close look at your finances and the goals for the future, you can find the right policy that best fits your needs and offers your heirsŌĆéthe protection they need. A financial advisor can also be useful in navigating the intricacies of life insurance so that youcan make an informed decision. -

Finance

FinanceTypes of Loans: A Comprehensive Guide

Loansmust be the mainstay of personal and business finance, helping individuals and organizations fulfill theirŌĆéaspirations. Loans allow access to money when needed ŌĆö whether it be for a newŌĆéhome, funding a business, or handling surprise expenses ŌĆö that can be paid back in installments. But not all loans are createdŌĆéequal.The future financial decision we will makeŌĆéis based on the type of loan we can take. This article covers the different types of loans, their purposes, and theirmain characteristics.1.Personal LoansIn a personal loan, borrowers receive a lump sum of funds to return in fixed monthly payments overŌĆéa set period of time, often one to seven years.The interest rates for personal loans can vary greatly on the credit rating, income, and repayment recordŌĆéof the borrowing individual.Personal loans provide flexibility but tend toŌĆécarry higher interest rates than secured loans.2.Mortgage LoansMortgage loanisa type of loan that is used specifically to purchase real estate (i.e. to buy a home or aŌĆéproperty), as opposed to personal loans. These are secured loans, meaningŌĆéthat the property in question is used as collateral. Because mortgages can represent an, if not the, largest monthly financial obligation anyone assumes, borrowers should study their budget andlong-term plans carefully before signing on the dotted line.3.Auto LoansAuto loans are loans for the purchase of a newŌĆéor used vehicle. Auto loans are also secured,ŌĆéjust like mortgages, using the automobile as collateral. If the borrower does not make payments, the lender can takeŌĆéback the car. Auto loans usually have shorter repayment periods, anywherefrom three to seven years, and they come with competitive interest rates. The loan amount is usually based on the price of the vehicle,ŌĆéthe borrower's creditworthiness and the down payment. Autoloans area common option for those who require reliable transportation but cannot afford to purchase a vehicle upfront.4.Student LoansHigher education is often expensive and itŌĆéis the purpose of student loans to assist individuals finance their college costs for tuition, books and those bit more expensive living expenses. These loans may come from the governmentŌĆéor private lenders. Federal student loans tend toŌĆéoffer lower interest rates and more flexible repayment options than private loans, such as income-driven repayment plans, graduated repayment plans, and possible loan forgiveness.Private student loans, by contrast,ŌĆécan carry a higher interest rate and far fewer protective provisions for borrowers. Student loans are unique becauseŌĆéthey usually do not need to be repaid until after the borrower has graduated or dropped out, making them an easy option for many students.5.Payday LoansThey are known as payday loan and are high interest loanŌĆédesigned to be paid back with a borrowers next paycheck. These loans are usually for small amountsŌĆéand intended to cover emergency costs. Payday loans, as previouslyŌĆémentioned, have astronomically high interest rates and fees, meaning they can be a dangerous choice for those borrowing money. Many financial experts recommend payday loans only if there are no other options, because they can start a cycle ofŌĆédebt if not paid back immediately.Borrowings are financial weapons that can work for or against youŌĆébut come at a cost.Each of this type serves a unique purpose and has its own associated terms, interest rates,ŌĆéand risk-sustainability. Before borrowing, it's important to evaluate your financial essential, shop around andŌĆéhave an understanding of the long-term ramifications of taking out a loan. That will help you toŌĆécreate informed decisions based on your needs and to have a secure financial future.From buying a home to funding an educationŌĆéto starting a business, the right loan can be an important steppingstone toward success. -

Finance

FinanceLower Premiums on Property Insurance: A Path to Financial Relief and Security

Importance of property insuranceis an essential aspect of financial planning that protects you from unexpected events like theft, naturalŌĆédisasters, or accidents. The cost of premiums has now become a hugeŌĆéburden on homeowners and businesses. Reducing premiums on property insurance can be a much-needed financial relief for those affected while ensuring they also have adequate protection in place toŌĆémaintain their livelihood and property. In this article, we will discuss how lower premiums benefit you, ways to get lower premiums and how that affectsŌĆépolicyholders and the insurance industry.1.Lower Premiums areŌĆéBeneficialReducing property insurance premiums dramaticallyŌĆéaffects household budgets and the way businesses are run. Lower premiums for homeowners result in higher disposable income that can then set aside for other necessary matters, whetherŌĆéit be education, healthcare, or savings. For businesses, reduced insurance costs can help cash flow and allowŌĆéreinvestment into growth initiatives or employee benefits. Moreover, competitive rates allow a larger segment of the population to afford coverage,ŌĆéresulting in fewer uninsured assets and increased financial stability overall.2.Strategies to Lower PremiumsInsurers typically use risk level of a property to establish premiums. For example, policyholdersŌĆécan demonstrate to their insurer that risk has been mitigated if risk mitigation measures like security systems, fire alarms, and storm-resistant features have been implemented ŌĆö possibly qualifying them for a lower premium. The upkeepŌĆéand improving the quality of the property must be maintained and can foster a safer premise, which, in turn, is another factor that can keep insurance costs low.Bundling Policies: Insurers often offer discounts if you bundle multiple policies withŌĆéthem, such as home and auto insurance. This streamlines theŌĆéinsurance process as well as saving substantial amounts on premiums. To get the most bang for the buck, policyholdersŌĆéshould inquire about bundling with their insurers.Raise Your Deductibles: Increasing the deductible, the sum theŌĆéinsured person must pay out of pocket before insurance coverage becomes active, can result in decreased premiums. This route, while generally more sound than merely denying the expense, simply requiresŌĆéyou to weigh your ability to absorb sudden out-of-pocket costs against the ongoing cost savings insurance benefits can provide.Shopping Around: The insurance market is very competitive, and prices canŌĆévary widely among providers. Policyholders shouldŌĆérepeatedly compare quotes from other insurers toensure they get the very best rates. Using online comparison toolsŌĆéand independent insurance agents can help make this process easier.Discounts and Benefits of Loyalty: Some insurers offer discounts if you've been with them for a long time, or if you'veŌĆémade few or no claims. Policyholders should ask about such perksŌĆéand use their loyalty to haggle for better rates.Property-specific Insurance: If a property owner makes a significantŌĆéinvestment in safety features, some insurers may offer discounts on premiums. These programs couldŌĆélower premiums while strengthening community resilience.3.Wider Implications for theInsurance IndustryItŌĆéis not only good for policyholders but also creates range for the insurance industry to further take benefits of it. Indeed, if insurers can help make insurance more manageable, they can increase their customer reach whilst decreasing theŌĆévolume of uninsured or underinsured properties. ThatŌĆéultimately reduces the cost burden on governments and communities during disasters. But insurersŌĆéneed to balance affordability and sustainability. Lower premiums should never involve sacrificing coverage or theŌĆéviability of insurers. By offering cost-effective solutions,ŌĆéthrough preventing measures or technology-based risk assessment, insurers can maintain profitability with innovative approaches.In summary, declining rates on property insurance are a win-win for policyholders and insurersŌĆéboth. TheyŌĆébring stability to the insurance marketplace, as they provide financial support to homeowners and businesses, promote wider access to insurance, and incentivize mitigation and risk management. Incorporating risk mitigation, policyŌĆébundling, and frequent market comparisons can lead to impressive savings for both individuals and companies. With manyŌĆénew entrants offering competitive rates, the insurance industry faces a challenge in building customer loyalty as well. This creates a society that is safer and more resilient, allowing property owners to insure their assetsŌĆéwhile also ensuring that it fits their financial needs. -

Finance

FinanceDifferent Types of Finance

Finance is the scienceŌĆéof funds management which studies in the management, creation, and study of money and investments.It is significant in both personal and organizational decision-making, affectingŌĆéthe allocation and utilization of resources. There are different types ofŌĆéfinance, each serving a particular purpose. It is crucial for individuals, businesses,ŌĆéand governments to comprehend these classifications as they navigate their financial path.1.Personal FinancePersonal finance is common and mostŌĆérelatable type of finance. It dealsŌĆéwith how to manage all of an individualŌĆÖs or a familyŌĆÖs financial resources ŌĆö budgeting, saving, investing, retirement planning. Other areas of personal finance include the management of debt (student loans, credit cards, mortgages) as well as financial security throughŌĆéinsurance and emergency savings. Personal finance is about creating a plan and managing yourŌĆémoney (how to allocate all your money) to reach your lot of money and avoid debts to achieve financial stability and long-term goal.This calls for prudent planning, consistency, and knowledge of financial productsŌĆéand markets.2.Corporate FinanceThe other one ŌĆöcorporate financeŌĆöfocuses on the financial activities of individual businesses and organizations. Involves managing a companyŌĆÖs capital structure, funding operations, and only investing in projects generating greater return than theŌĆécost of capital. Corporate finance involves the activities related to raising capitalŌĆöwhether through equity or debtŌĆöcash flow management and project or acquisitionŌĆéanalysis. It is the job of financial managers within corporations toŌĆéjuggle risk and return (so that the company does not become so risky that the business is unsustainable in the long term). This kind of financing is a vital component for companies of allŌĆésizes, small start-ups to multi-national companies.3.Public FinanceAnother key area of coverage fromŌĆéthe financial world is public finance. It includes all aspects of revenue generation through taxation and other methods, and the distribution of resources for programsŌĆélike education, health care, infrastructure and defense. Public finance encompasses the management ofŌĆépublic debt and the overall fiscal health of the economy. It is only in this context, that it becomes possible to make decisions that can be strategic, as governments are only now focused on how they can best support and fulfill the needs of their people while balancing economic growth against theŌĆérealities of a surplus-less economy in the near future. Finance that is heavily linkedŌĆéto economic policy and the economy.4.Investment FinanceInvestment finance deals with theŌĆéorganization and management of investments and portfolios. This includes studying financial markets, various risk levels, and where bestŌĆéto put your money for the best outcome. Such finance plays a crucial role forŌĆépeople and organizations wanting to increase their wealth over time.5.International FinanceInternational finance are transactions made in one country and intended to be paid forŌĆéin another. It involves a range of subjects like foreign exchangeŌĆémarkets, international trade, cross-border investments, and global economic policies. This is critical for any business operating in a global environment where international finance can play a major role in determining financial decisions domestically, with currency fluctuation,ŌĆétrade regulations, and geopolitical risk. It is also greatest importance for global economic stability, as countries dependŌĆéon international financial systems to support trade and investment.6.Behavioral FinanceBehavioral finance is a newerŌĆéfield that combines psychology and finance to understand the effects of human behavior on financial decision-making. WhyŌĆépeople and markets sometime do funny things and build phenomena like bubbles (bubble in stock market), live in denial or take way too much risk, etc. Behavioral finance aims to explain why these behaviors occur and how to minimize their effects onŌĆéfinancial outcomes. Data of this nature can provide invaluableŌĆéinsights into market behaviour as well as enhancing financial decision-making.ToŌĆésummarize, finance plays a big part in the world and the types are good for serving different purposes. From personal savings, business management, nation governance to market investment and globalŌĆéfinancial system understanding, each finance type is important to explore. KnowledgeŌĆéabout these categories will help the individual and organizations take accurate decisions and reach their monetary objectives. -

Finance

FinanceCredit Unions Offering the Best 5-Year CD Rates

Certificates of Deposit (CDs)ŌĆéare a popular choice for those saving money. Out of all the different CD terms available, 5-year CDs tend to have some of the highest interest rates, so they are often a good option for investors who are willing to tie up their cash forŌĆéa longer duration. Banks tend to be the default choice for CDs, but credit unions have come to be a strongŌĆéalternative, frequently offering competitive rates and member-centric perks. This article explores credit unions that are offering some of the best 5-year CD rates and whether they are the right option for your savingsŌĆéneeds.1.Navy Federal Credit UnionNavy Federal Credit Union (NFCU), in fact, is one of the largest credit unions inŌĆéthe USserving military members, veterans and their families. NFCUŌĆéis a competitive player on CDs as evidenced on its 5-year CD. Currently, the 5-year CDrates with them are frequently among the highest available on the market. Besides competitiverates, NFCU offers flexible terms and the option of a specialty certificate that gives it a one-time rate bump during the term. Membership is limited to military or Department of Defense affiliates, but for thosewho meet that criterion, NFCU is among the very best.2.Alliant Credit UnionAlliant Credit Union is a name that you can trust on this list with their competitive rates andŌĆéalso high-yield CDs. Ally's 5-yearCD is especially attractive for anyone who wants to make the most of their savings. Alliant also has low fees and an easy-to-use online bankingŌĆéplatform, making it a great option for tech-savvy consumers. Anyone who joins Foster Care to Success, a nonprofit organization, canŌĆébecome a member for a small donation.3.PenFed Credit UnionAnother one ofŌĆéthe best 5-year CDs comes from PenFed Credit Union ŌĆö short for Pentagon Federal Credit Union. Originally catering to military personnel, PenFed has opened its membership toŌĆéanyone who joins a qualifying organization or donates a small amount to a partner nonprofit. Consistently competitive with PenFed 5-year CD Rates, they offer a variety of CDŌĆéTerms for your investment goals. They provide easy access to online tools and resourcesŌĆéto help you manage your account and track your savings progress.4.Delta Community Credit UnionGeorgia-based Delta Community Credit Union is one of the Southeast's marqueecredit unions, and it offers some of the best CD rates you can find in the region. One of their most attractive products is the 5-year CD, which frequently offersrates that beat many of the national banks. Membership is available for residents and people who work, worship or go to school within eligible Georgia counties, as well as select employer groups andŌĆéassociations. Delta Community also offers customer service excellence and diverse financial products to meet needs acrossŌĆéthe spectrum.5.SchoolsFirst Federal CreditŌĆéUnionSchoolsFirst FCU is one of the largest credit unions for school employees inŌĆéCalifornia and offers some of the best CD rates. Contributing to its popularity is their 5-year CD forŌĆémembers looking for a long-term saving solution. SchoolsFirst also has a broad range of CD terms and an option to ladder CDs, which enables members to stagger when the investments mature for greaterflexibility. Membership is limited to the educationŌĆéfield, but it's a great option for those who qualify.In conclusion, individuals looking for the best 5-year CD ratesŌĆéwould do well to check out credit unions. Credit unions such as Navy Federal, Alliant, PenFed, Delta Community and SchoolsFirst drive the top tierof competitors with their member-oriented focus, competitive rates, and community-driven values. However, by analyzing your financial targets and comparing the services offered by different credit unions, you can discover a 5-year CD that enables you to grow your savings alongside anestablishment that prioritizes the needs of its customers. If you're saving for something big, an emergency fund, or a retirement fund, then a 5-year CD offered by a credit union mayŌĆébe just the tool you need to reach those goals. -

Finance

FinanceChoosing the Best Financial Adviser: A Guide to Securing Your Financial Future

With time going by, one's financial goals become more and more complex, therefore, we need someone professional to help us manage our finance. A financial adviser can help, whether you're planning for retirement, saving for a big purchase or investing for long-term growth. Not every financial adviser isŌĆécreated equal, though. Here's a completeŌĆéguide to choosing a financial adviser who is best suited to your needs.1.Familiarize Yourself with YourŌĆéFinancial GoalsThe firstŌĆéstep toward finding a financial adviser is to clarify your financial goals. Do you want to build wealth, pay down debt, or save for retirement or your child's college education? Different advisers will have different specialities, soŌĆéif you're clear on what you want to achieve this will help you think about what types of people you might need. If retirement planning is your priority, you will want an adviser who specializesŌĆéin pension plans and long range investing strategies.2.Verify Credentials and ExperienceThe credentials a financial adviser has and how many years of experience they have inŌĆéthe business are important markers of expertise. Seek certifications such as CERTIFIED FINANCIAL PLANNER (CFP), Chartered Financial Analyst (CFAs), or Certified PublicŌĆéAccountant (CPAs); These designations require substantial training, and there are professional standards behind them,ŌĆébut no bar exam or certification as there is in law. Also, ask howŌĆélong the adviser has been in the industry. The healthier the body, the more capable you are of developing muscle, realizing that your newŌĆéactions and the fat burning process soon are the results of habit and time.3.Evaluate Their Fiduciary DutyA fiduciary, by law, is required toŌĆéact in your best interest ŌĆö putting your needs ahead of their own. That means they putŌĆéyour best financial interest ahead of the commissions or fees they might earn. AlwaysŌĆéask if the adviser is a fiduciary and, if necessary, ask for written confirmation.4.Get a Grip on TheirŌĆéFee StructureFinancial advisers may be compensated in a number of ways, but the most common areŌĆéfees, commissions or a mix of the two. Flat-fee, hourly or percentage of assets under management fee-only advisers may be less prone to conflictsŌĆéof interest. Commission-based advisers earn their money from selling financial products, andŌĆétheir sales may not be in your best interests. Ask aboutŌĆétheir fee structure upfront and make sure that it's clear and reasonable.5.Check out TheirŌĆéCommunication StyleGood communication is paramount to a successful adviser-client relationship. Your adviser should be able to distill complex financial concepts in an understandable way. They should also be available and responsive to your questions and concerns. In those initialŌĆémeetings, look at whether they listen well and if they personalize advice to your particular circumstances.6.CheckŌĆéout Reviews and Ask for ReferencesWhen choosing a financialŌĆéadviser, reputation matters. View the online comments or testimonials, or ask for references and suggestions from previous clients. This can help you judge whether they are reliable and professional. Don't be shy about requesting case studies or other examples of how the adviser has worked withŌĆéclients with similar financial goals.7.Trust Your InstinctsFinally, listen to your gut feeling. Choosing a financial advisor that meets your standard and makes you satisfied is very important, because he or she determines how your financial conditions operate. If something doesn't feel right with your experience it's just fine to continue looking until you meet people who you connect with.In short, hiring a financial adviser may be one of the mostŌĆéimportant decisions you ever make in the course of managing your finances successfully. Knowing your goals, researching credentials, verifying fiduciary duty and testing communication styles will help you find an adviser that aligns with your needs andŌĆévalues. Take your time, ask a lot of questions and remember that the right adviserŌĆéwill do more than help you manage your money, they will empower you to reach your full potential financially.

Trending┬ĀArticles

-

Finance

FinanceTaking a Mississippi River Cruise: An Unforgettable Experience

The Mississippi River can be said toŌĆébe a living history book, reflecting the story of America ŌĆö its past, present and future ŌĆö and to cruise on it is to know American culture as well. From its headwaters in Minnesota to its mouth at the Gulf of Mexico, this serpentine river is more than 2,348 miles long and, with its many tributaries, provides the ultimate scenic and culturallyŌĆérich road trip. But before you set sail, here are a few thingsŌĆéthat will make your cruise experience unforgettable.1.Get Familiar with the Itinerary and Call PortsMississippi river cruises have a variety of routes, withdifferent itineraries covering a range of interests. Some cruises sail the entire length of the river; othersŌĆéare tailored to specific sections, such as the Upper Mississippi, the Mississippi Delta or the picturesque St. Louis to Memphis stretch. Learn about the port itinerary, eachŌĆéport of call can provide different ports of calls. From dynamic city lights in Memphis to tranquil lands of the Upper Mississippi Valley, each port provides a uniqueŌĆéexperience of the region's culture and lifestyle.2.Choose the Right Cruise ShipMany cruise lines operate on the Mississippi, each with its own ships, amenitiesand vibe. Considerthe ship's size, cabin options, dining and entertainment optionson board, for example. Bigger ships might offer moreŌĆéopulent amenities and wider decks for magnificent river views, but small vessels can provide a more intimate and personalized experience. Look up theŌĆéreputation of the cruise line and check reviews so that you will choose a ship that matches your style.3.Plan Your SeasonDeciding on the best time to take a Mississippi River cruise mainly comes down to the type of weather andseasonal activities you want to enjoy. Spring and fall feature moderately ideal temps and fewer crowds, so it'syour best bet for a relaxed cruise. Summer means warmerŌĆéweather and more celebratory vibes, making it ideal for outdoor activities and music festivals. Winter cruises, though less common, can deliver a wonderfully peaceful and off-season experience, though you'll have to gearŌĆéup for cold-weather conditions.4.Pack SmartWhen packing,ŌĆékeep in mind that you'll be traversing both land and sea. Pack clothes that you can layer for changingŌĆéweather and comfortable walking shoes for port excursions. For warmer seasons, don't forget sunscreen, hatsand insect repellent. Pack a reusable water bottle ŌĆö it's important to keep hydrated during excursions on aŌĆécruise.5.Embrace the Local CultureThe Mississippi River is sewn into the fabric of AmericanŌĆéhistory and culture. From Delta blues music to Civil War history along the way, every port is a trove of stories andŌĆétraditions. Chances are, you will have the chance to take part in local tours, see culturalŌĆéperformances and try regional cuisine. Your cruise experience will be made brighter with some local culture time, and the memories willŌĆéremain for forever.6.Be Aware of RiverConditionsAlthough the Mississippi River is navigable in general, conditions on the river vary, particularly in times of heavyŌĆérain or drought. Stay updatedŌĆéon weather predictions and river heights to make sure your cruise is on schedule. Cruise lines usually watch these conditions closely and will change itineraries as necessaryŌĆéto ensure safety.To sum it up, a Mississippi River cruise is a one of a kind wayŌĆéto see the heartland of America. Knowing the route, selecting the right vessel, planning your season, packing appropriately, exploring local culture and remainingŌĆéaware of river conditions will contribute to a fulfilling cruise experience. Well, hoist your sails upon the grand ole river wee the mightyŌĆéMississippi and let the warm waters cadge you up on a course of rediscovery and delight. -

Finance

FinanceSteps to Get Discounted Airfares for Seniors

Regardless of age, traveling is something that many people love and for seniors, it can often open up new territory to explore, revisit their favoriteŌĆéplace, or get the opportunity to see the world at a relaxed pace. But sometimes the costŌĆéof airfare becomes an obstacle to those travel dreams. Luckily, there are plenty of methods seniors can take advantage of to save money on airfares, so their travels can be enjoyablewhile still being easy on the wallet. Here are very useful tips toenable you save more from your nextŌĆéflight.1.Become a Member ofŌĆéAARP and Other GroupsJoining associations, for example, AARP (American Association of Retired Persons) is one of thesimplest ways for seniors to receive concessions. There are a number of travel benefits with AARP, including exclusive airfare offers made possibleŌĆéthrough partnerships with airlines.A nominal fee typically comes with membership, but the savings on flights morethan offsets the expense. Watch AARPŌĆÖs travel page for flashsales and otherseniors-only offers.2.Use Airline LoyaltyProgramsMost airlines have loyalty programs that compensate frequent flying travelerswith points, miles,or cash discounts. As a senior, joining these programs and earning points from some occasional trips can help one save a good amount of money overtime. Some airlines also havespecial senior discounts, so itŌĆÖs worth reviewing the fine print of your favorite carrierŌĆÖs loyalty program forage-specific advantages.3.Book at the Right TimeAirfare is allabout timing. In general the best fares become available middle of the week (Tues or Weds) and several months ahead oftravel. During thesetimes, airlines often release promotional fares that seniors can capitalize on. Do not book during busy travel periods orholidays when rates can be sky high. Being flexible with your travel dates can alsounlock cheaper options.4.Use Travel Agencies, Websites that Specializein Senior DiscountsThere are plenty of travel agents and online sites which caterspecifically to offering seniors discounted prices. SeniorDiscounts.comand similar web sites have a great deal of information.Travelzoocan be excellent resources for deals. These platforms pullŌĆéoffers from different airlines,by doing this you can compare prices and choose the fittest option without going through many different airline pages.5.ExploreAlternativeAirlines and RoutesBudget airlinesand smaller carriers often aren't the first choice, but often offer the best value for money. Donot ignore these options if they service your destination.And, comparing other airports or layover pathscan yield huge savings as well. Occasionally a slightly lengthier trip can yielda considerably cheaper fare.6.Get a Dealand Ask for DiscountsFeel freeto contact airlines directly and ask about other possible senior discounts. Some airlines advertise their senior rates front and center, but others may haveŌĆéthem available only on request. Be courteous and persistent; a single phone call might getyou a substantial discount thatŌĆÖs notmentioned in plain view7.Utilize Companion FaresSenior travelers can find low-cost tickets by keying in specific keywords (such as oneof the benefits airline offerŌĆöcompanion tickets) in the airline website's search bar. If you are eligible for a companion fare, the price of your trip can effectively be cut inhalf. Look for such promotions that cango a long way in working wonder.To sum up, although airfare can discourage travel, older adults have a number of options to try to getreduced rates. With all above mentioned ways and methods such as understands joining the right organizations loyalty programs, closet brochure booking, travel-new-specialty-organizations, alternativetrips, negotiating, partnerships for two mates, you can get discounted airfares for seniors. -

Finance

FinancePlanning a Family Vacation: A Guide to Creating Lasting Memories

Planning a family trip canŌĆébe fun but also overwhelming. It's a chance toŌĆémake lasting memories, enrich relationships and break away from the daily grind. But designing a trip thatmeets everyone's interests and needs require a lot of planning and consideration. Whether you envision a beach getaway, a cultural adventure or an outdoor retreat, here's a complete guide to planning a family vacation everyoneŌĆéwill love.1.Plan Your Trip TogetherGet everyone involved in the first step of planning a successful family vacation by working together to makethe right decision. Gather as a family and discuss possible destinations,activities andŌĆébudgets. Give each family member an opportunityŌĆéto express what they would like to experience on the trip. Young kids maybe thrilled about theme parks, teens boom out on adventurous stuff like hiking or water sports. Parents may emphasize relaxation or exploring culturalŌĆésights. Getting everyone's input helps you to plan aŌĆévacation that will satisfy all ages and interests.2.Select theIdeal DestinationPicking the right destination makes up a large part of anyfamily trip. Take into account things likeŌĆéhow long it will take to get out there, the weather, and whether there are activities to do out there a family would like to have. If you're traveling with younger kids, you may want the place to beŌĆéfast and easy to reach, with plenty to see and do for kids. ForŌĆéthose with teens, maybe a place with adventure but also time out is best. Popular places for familyŌĆévacations include beach resorts, national parks and cities with rich cultural and historical experiences.3.Plan Activities Everyone Will Be Involved inAperfect family vacation walks the fine line of fun and relaxation. Once you have selected a destination, research activities and sights thatareinterest-specific. ToŌĆéillustrate, a beach trip may have swimming, sandcastle construction, and beach volleyball. When you travel to a city, you might visit museums, local markets, and liveŌĆéperformances. Make sure youŌĆéschedule some downtime so people can feel refreshed and energized.4.Prepare for the UnexpectedEven with all the planning in the world, problems can arise on aŌĆéfamily vacation when you least expect it. Flight delays, bad weather, andŌĆéeven minor illnesses can derail your plans, so you're going to want to be prepared. Have a fallback plan for activities if bad weather arrives, and pack a mini emergency kit with band-aids, pain relievers and a portableŌĆéphone charger. Flexibility and a good attitude are everythingŌĆéwhen things don't go as planned. The ideaŌĆébeing quality time together as a family.5.Record the MomentsThis is why a familyŌĆétrip is the perfect opportunity to make lasting memories. We used a camera to snap picturesŌĆéand videos of our travels. Be sure to write things down in a travel journal or scrapbook there will be souvenirs to help jog your memory of the fun time you had and you can have fun together when youŌĆéwere traveling.6.Reflect and ReconnectSpend some time after the vacation discussing asŌĆéa family about the experience. Tell about your highlights and whatyou learned from the trip. TakeŌĆéthis time to strengthen family ties. To the contrary, planning a family trip ŌĆö and having fun on one ŌĆö can hit both those notes and leave you with memoriesŌĆéyou'll cherish for a lifetime.To sum up, organizingŌĆéa family holiday takes a lot of time and effort, but the best part about it is really worth it. Involve everyone in the planning process, create a budget,pick a suitable destination and be ready for the unexpected, to ensure a fun and memorable trip for the whole family. Go ahead and plan and pack your family adventure today and prepareto create lasting memories.

Featured┬ĀArticles

-

Travel

TravelTop Tips for a Perfect Day at Universal Studios Hollywood

-

Travel

TravelTop Attractions to See in Yellowstone National Park

-

Health & Wellness

Health & WellnessUnderstanding Spinal Muscular Atrophy: Recognizing the Key Symptoms

-

Health & Wellness

Health & WellnessImportant Actions to Take When Being Diagnosed Spinal Muscular Atrophy

-

Automotive

AutomotiveWho Should Consider Renting from U-Haul?

-

Automotive

AutomotiveThe Real Cost of Renting a U-Haul in 2026: Beyond the $19.95 Sticker

-

Finance

Understanding the Core Components of a Reverse Mortgage Calculator

-

Finance

Securing Your Golden Years: A Guide to Top IRA Accounts for Retirement Savings